Dallas Fed: Real estate could face ‘severe price correction’

Soon after, wealth spoke to Dallas Fed economist Enrique Martínez-García. While the pandemic housing boom isn’t the same story as the prequel to the housing crash of the 2000s, he said, house prices quickly decoupled from underlying fundamentals.

“This could be a real estate bubble. The evidence suggests it looks like a real estate bubble. A bit like a duck. It walks like a duck, it looks like a duck, it could certainly be a duck,” said Martínez-García wealth in May. “[It’s time to] Awareness of possible risks [that] housing poses.”

Fast forward to February 2023, and Dallas Fed economists are again warning about downside risks in US and European housing markets, which have already slipped into slumps after central bank rate-hiking cycles began in 2022.

“While home price growth has recently started to moderate — or in some countries, slowing — the risk of a deep global housing meltdown remains,” Dallas Fed economists wrote on Tuesday. “Affordability crises often arise from unsustainable and widespread exuberant behavior, data shows. Of particular concern is that housing has become more vulnerable to cross-border excesses, leading to significant resource misallocation and efficiency losses.”

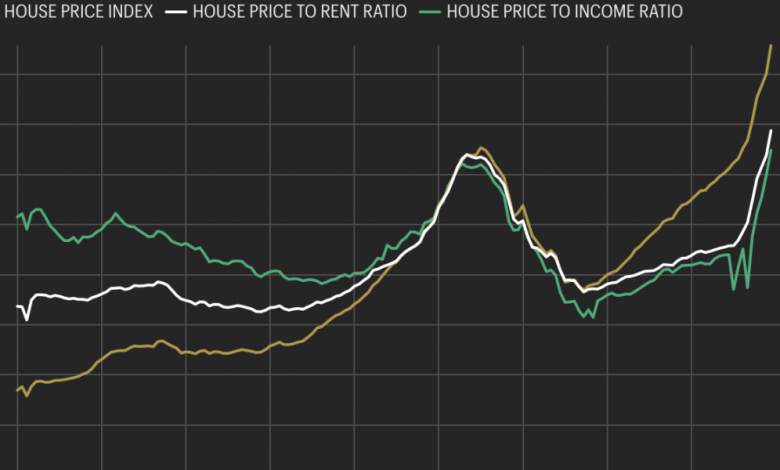

According to analysis by economists at the Dallas Fed, in 2022 the US price-to-income ratio surpassed its peak reached at the height of the housing bubble in the 2000s. Unlike in 2008, this time we don’t have a subprime crisis or a glut in housing construction. However, economists at the Dallas Fed say US home prices can still fall.

“Achieving a soft economic landing — taming inflation and avoiding a recession, as the Fed accomplished in 1994 — cannot be taken for granted, as further monetary tightening increases the burden on household mortgage debt and increases the likelihood of a severe home price correction,” Dallas Fed economists wrote.

To “bring the United States into line with theirs [housing] Fundamentals,” Dallas Fed economists say US home prices should fall 19.5%. While Dallas Fed economists are hinting at the possibility of such a deep decline, it doesn’t look like that’s their baseline forecast.

“While a modest housing correction remains the base case, the risk that tighter-than-expected monetary policy could trigger a sharper price correction in Germany and the US cannot be ignored,” Dallas Fed economists wrote in their latest article.

According to her research, countries across much of the developed world saw house prices detach from underlying fundamentals during the pandemic real estate boom. But in her view, the “bubbly” real estate markets in the US and Germany could pose the greatest economic risk to the rest of the world.

“The US and Germany pose a significant risk to global housing because of the size of their economies… The possibility of a domino effect, with investors pulling out of international housing to seek safety and liquidity elsewhere, also raises concerns about encroachment over it out to Germany or the US into the global economy,” wrote economists at the Dallas Fed.

Through December, U.S. home prices, as measured by the seasonally adjusted Case-Shiller National Home Price Index, are down 2.7% from the June 2022 peak. While this is the second largest price correction in the series, dating back to 1987, it pales in comparison to the 26% peak-to-trough plunge in home prices observed between 2007 and 2012.

Simply put, so far, rising mortgage rates have resulted in only a modest home price correction, with some markets having little impact.

But let’s assume we slip into what the Dallas Fed calls a “more serious price correction” scenario. If that were to happen, it’s still unlikely to match what we saw after the 2008 housing crisis and subsequent foreclosure crisis.

“Despite the risk, one material correction As for home prices, several factors are helping to allay my concerns that such a correction would trigger a wave of mortgage defaults and potentially destabilize the financial system,” Fed Governor Christopher Waller told an audience at the University of Kentucky in October. “One is that because of the relatively tight mortgage lending in the 2010s, the creditworthiness of mortgagors is generally better today than it was before this last real estate correction.”

Want to keep up to date with the US housing market? Follow me on Twitter at @NewsLambert.

Learn how to navigate and build trust in your organization with The Trust Factor, a weekly newsletter exploring what leaders need to succeed. Login here.